|

2/13/2017 being safe onlineWe now live huge chunks of our lives online, and do ever more of our financial transactions and interactions via email, applications on our phones, and through websites. As a provider of financial planning and investment advice, I am perhaps a little more sensitive than most to what can go wrong in terms of online security and privacy. The recommendations below are not intended to be comprehensive or "fail safe", but could form a foundation for improving online safety. lock your phoneThis one should be obvious, but it seems that a number of us out there in the world are still resisting the step to add a PIN, fingerprint, or password to our smartphone. These devices typically have unrestricted access to email, social media, and maybe even financial accounts via apps. Accidentally leaving an unlocked phone on the bus, coffee shop table, or a park bench can provide one-stop access to a stranger. At a minimum, a 4 digit PIN or "pattern lock" can provide a measure of protection, especially against the mildly curious. BONUS: take a minute to review the "remote lock" function for your phone model, operating system, or carrier. iPhone Remote Lock Instructions Android / Google Remote Lock Instructions go two factorAn increasing number of accounts (email, Facebook, Twitter, etc) offer what is called "two factor" or "two step" authentication or log-in. What this means in brief is that to initially access your account on a new device (phone, laptop, tablet) you must have both the password AND a code sent to a trusted device. So you may be logging into Gmail on a new computer and Google will send a text message to your phone, adding a layer of security to that log-in. Generally, you can choose to have your account "remember" that device, so you do not have to go through the two step process every time. HOWEVER, if you are using your phone as a part of this two step process, it becomes even more important to password protect or otherwise lock your phone. passwords are crucial The first line of defense against another person accessing private accounts may just be having a decent password. Gone are the days of being able to pick a pet's name or a clever but simple combination of initials and birth date. And it is not reasonable to use the same password for multiple services. Current best practice in strong passwords require length and randomness. One approach could be a string of 8+ random numbers, letters (both lower and upper case), and symbols. A challenge with this option is that the password can be overly difficult to remember even one account, much less a similar string for dozens of accounts. A second option can be a "phrase" or combination of random words: "bananaumbrellafloristdog" is an example that may work in some scenarios...throwing in a number or symbol would make it better. Using a "password manager" may be helpful for some people, or having a readily accessible (but secure!) reference with various passwords could be supportive. browse awareSome browsers (the software you use to access the internet) now default to a "secure" mode when possible. You can check whether your access is in this secure mode or not by looking at the address bar. The actual language or graphic varies by browser, although most will show some version of a "lock" and include the letters "HTTPS"; an example from Chrome is in the image below. To be clear, being in "HTTPS" vs "HTTP" does not guarantee against invasions of privacy or remove any personal responsibility for security, but is better on a relative basis.  10/6/2016 is it bad to die with $0 left? I think it is pretty common for people to fear "running out" of money. We've all heard stories of people "dying broke" or reduced to poverty late in life, and those stories are both sad and scary. So it makes a great deal of sense to avoid that fate. Financial planning and prudent investment management play a crucial role in an overall approach to help ensure there are sufficient assets and income in place as we age, and they can also help prevent having too much left over as well! how can there be too much money?If we all agree to the premise that it is generally not comfortable to run out of money during our lifetimes, it may then seem counter-intuitive to discuss the opposite challenge of dying with too much income or assets. But prudent personal financial management also involves making a plan for the eventual distribution or transfer of an estate, as well as the care of the people and causes that have mattered to the person during their life. A well crafted financial plan will seek to find an appropriate balance between having too little and having too much. quick look at "too much"What happens when you die with "too much" in terms of assets?

what's the plan?The points above are meant to highlight that, while having assets and income is probably a better state of affairs for most people than having none, it is also the case that having significant assets and income involved demands careful planning as well. A robust financial plan with a qualified financial planner, such as a CFP®, should seek to address both ends of this question, from dying with too little to dying with too much, as well as a number of other important financial considerations. Ready for more information?Click the "let's talk" button to send me an email. I am a fee-only, registered investment advisor offering highly transparent financial planning and investment management advice in a fiduciary context.

10/4/2016 exploring the emergency fund

It's not always easy to get a bead on exactly what "normal people" understand about their finances. I tend to frequent public blogs and forums (places like Reddit and Quora) where people discuss personal finance best practices and strategies, as well as industry "insider" newsletters and trainings about investor psychology and behaviors. My top level impression is that most people have a pretty decent, general idea of "personal finance": save some money, invest for the long term, try not to overpay for advice.

One very basic part of every financial plan, and one that tends to be reduced to a simplistic rule, is the "emergency fund". It could also be called "cash on hand" or "liquid funds" or something similar, but the idea is the same: this is a stash of money set aside from the monthly budget (it shouldn't be spent down and replenished in a "normal" period) and that it mostly held in a very low risk way (checking or savings account at the bank is very typical); the purpose of this money is to cover extraordinary expenses or demands on the budget to prevent serious disruptions to regular bills, lifestyle, and use of credit. It is impossible to know the future with certainty and to plan for ever possible eventuality, but it is possible to plan for a series of reasonably likely demands on the household budget (as suggested in the picture above). So that explains in general terms what the emergency fund is, but leads to the more practical questions around where does this rank among goals, how much is necessary , and how to hold the funds.

the emergency fund is a priority

Every person and every household have different specific needs and challenges, but everyone engaged in the process of financial planning is going to share in some measure this goal of having cash set aside for budget shocks, and that goal is going to be very near the top of their list of priorities (or should be). "Cash flow" may not sound sexy, but once the flow of cash through a budget is pinched, everything else financial becomes very difficult to manage. For that reason, in my planning and investment advisory work with clients, we focus on addressing this goal early and revisiting it often as life changes impact the answer to the how much question. And speaking of...

the "rule of thumb" is a starting place - Not an end to the conversation

If you were to Google "emergency fund amount" or "how much do I need in savings for emergencies" you will likely find a number of sources pointing to a rule of thumb suggesting "three to six months of expenses". And that is totally a reasonable place to start the conversation, provided that person's budget is pretty stable to begin with and they earn more than they spend on a regular basis. But this is only a starting place for the conversation, because the details in peoples' lives vary so much. Here are some considerations that could move a given person's emergency fund needs up or down significantly:

consider a tiered approach to risk

Having money in an emergency fund but not being able to access it in an emergency renders the whole exercise pointless. With this in mind, it makes sense to consider liquidity and risk for how those funds are held. Some people may wish to consider a "tiered" approach to holding or investing their emergency fund, particularly people with a relatively high dollar amount allocated for this purpose.

review, revise, pivot

To wrap this up with one more piece of practical insight: The amount set aside of emergencies should be informed by each person / household's actual circumstances and exposures, and these should be reviewed periodically for fit. When things change, the emergency provisions should also change. In some cases, the "emergency" turns out to be the new status quo and things must be adjusted more dramatically for the long term; for example, a "short term" unemployment may turn out to be more permanent, and the emergency fund alone will not defend the existing budget and financial goals. Or on a more positive note, people who find themselves with total wealth and income far outstripping their potential needs may choose to stage themselves out of holding a reserve account.

Ready to do some planning?

If conversations like this one pique your interest and you are ready to dive deeper into planning your own finances, email me at David@DRWFinancial.com. I am registered as an investment adviser in the states of Tennessee and Georgia, and may provide advice to residents of 46 other states under certain circumstances (no TX or LA at this time). Or for a quick review of your current situation, feel free to click the following buttons:

Quick and free risk analysisSimple retirement goal check-up Budgeting tends to be a consistent area that people struggle with in their personal finances, whether or not they work with a professional adviser. In my experience, I've found that one of the primary stumbling blocks along the way to a workable budget is the desire to work backwards. there is a logic to the orderThe first step to developing a budget is to identify current spending, but too often we start by trying to justify our spending. What's the difference?

To be clear, there is no judgment here about each person's justifications, but rather a suggestion that building a budget backwards by justifying current spending and wants will often lead to an overspent or under-considered budget. But approached the other way, with a clear picture of where the money is going each month, which categories get the most and least money, and what patterns are apparent, you now have the ability to single out which items most need to be justified, and what it will take to make it fit the overall budget. how to begin?There are tons of apps and worksheets and systems out there to help people with budgeting, but my absolute favorite and most simple option in the days of electronic banking and online credit card accounting is to download your spending history directly from your bank and credit card companies in a spreadsheet. They will most likely have things grouped in categories already, but it is a simple thing to add a new column and sort your stuff into groups you find useful.

I recommend starting with no more than four to six categories and putting every line item into one or another. That's where you start! 1/12/2016 on being differentHow is DRW Financial different from our competitors? How do we aspire to be worthy to provide advice and investment management to our clients? These are good questions, and deserving of an answer. Below and in brief I will outline my philosophy and the DRW Financial approach to delivering service. self sorting?One key to our approach in identifying prospects and taking on new clients relies on the concept of self sorting. We believe that the best client relationships arise when the clients themselves see us as a good fit, as opposed to being "sold" on our services. In some ways this is like going on a few dates before committing to a longer term arrangement. And the process relies on both parties -- if DRW Financial doesn't get the sense that we can productively work together, we will (and have!) refer prospects on to another professional who seems like a better match. Values before moneyWhen a prospect does become a client, our early work is dominated by a conversation around values, specifically the values that inform the client's life. In some cases, clients have yet to take the time to articulate their thoughts and priorities around their value system, and David & DRW Financial serves to facilitate that conversation. We aspire to remain agnostic, not imposing our values onto our clients, but choosing instead to be good and discerning listeners. fiduciary means clients come firstDRW Financial is organized as a registered investment advisory. Our sole compensation comes from the delivery of advice via a financial planning fee or a fee only investment management fee. RIAs must adhere to a fiduciary standard. The combination of this standard and our compensation arrangements create a scenario where our interests align with those of our clients, as well as providing simple transparency to identify conflicts of interest where they may exist. simplicity and transparencyWhen we deliver advice or design investment portfolios, we aspire to high standards of simplicity and clarity. While there are complicated concepts in the world of finance, we believe that good advice should be understandable and actionable. We avoid "black box" investment products; we favor planning that follows best practice; we design plans and investments to be portable should our clients wish to transition to a DIY model. Our portfolios tend to be rely heavily on low cost "index tracking exchange traded funds", individual stocks, and bonds. cooperation, not competitionWe work alongside our clients in pursuing their goals. We are also open and willing to working cooperatively with other members of the "team" advising our clients: estate planning attorneys, tax professionals, insurance agents, and similar all have roles to play and DRW Financial is able to productively engage with each. In circumstances where our clients need services not directly provided by DRW Financial, we are able to provide objective and conflict free advice on how and where to find those services. technology forwardDavid and DRW Financial are committed to communication. We make use of personal interaction, the telephone, email, and social media to engage with our clients, and we leverage a select set of technology platforms to support our values of simplicity and transparency. Different clients have different needs, and our technology suite is curated to allow for a variety of modes of engagement. On one point we remain proudly abnormal: David answers the phone and responds to emails directly, and with an efficiency many clients find startling. professional developmentDavid brought more than a decade of financial services experience and education to DRW Financial, and since founding the firm has sought and earned designations as Chartered Advisor in Philanthropy® and CFP®. Our intention is to continue seeking new learning and evolving our approach along with industry best practice. questions to askWhen you find yourself evaluating the options for choosing professional financial advice or going the DIY route, you may wish to consider the following (with notes on our likely answers):

11/17/2015 reflectingIt was around this time of year back in 2012 that I gave notice to my managers that I was leaving their employment to start my own business. After twelve years in a couple of roles there, I felt that I had fulfilled the opportunity available to me, had delivered considerable value, and was ready to focus more on pulling my work life into alignment with my core values. Family | community | legacyWhen I created my firm, I worked the words "family, community, legacy" into my logo; while the words mean a range of things to different people, to me they captured what I am working toward in my personal and professional life. I want to care for and support my own family, and I want to help other people do the same on their terms. I want to be an engaged contributor to the health and well being of my community, and to facilitate the work of other people and organizations in their unique approaches to that same mission. And I want to do all of this in full awareness that whatever we do now has the potential to create long term echoes and impacts, thereby shaping a legacy. progress...and work to be doneThree years ago I walked away from what seemed like a pretty good gig, and there are definitely things I miss: the money wasn't bad, I had a significant degree of autonomy in how I ran my desk, and I had the confidence of knowing that I was good at my job -- but what I miss the most are the relationships with the people I talked to daily or weekly. There were people who worked alongside me, clients that I served, and professionals at other firms with whom I negotiated / traded / swapped insights, and all of them contributed a lot to my personal growth. But just as I miss some things from that time in my life, DRW Financial has allowed me to focus on a much smaller set of clients, and this focus has led to what I believe to be is a higher quality approach to managing the specific and varied needs of those clients.

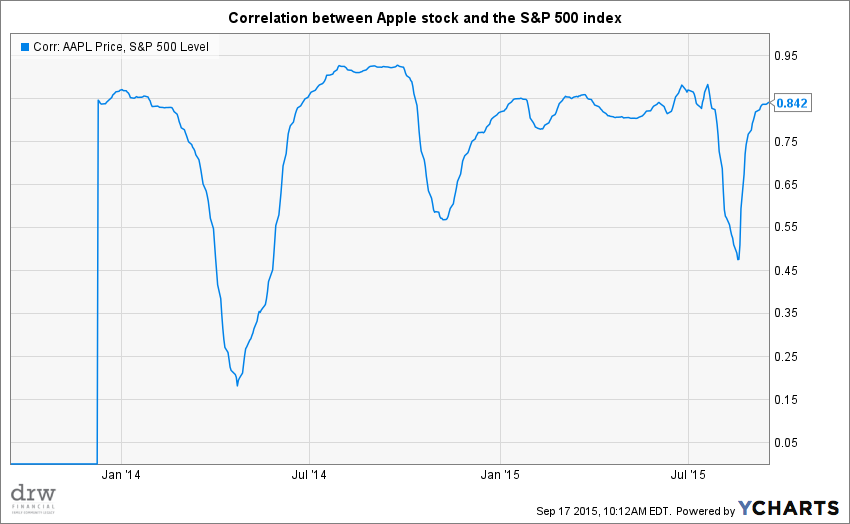

I am about halfway to my target for size and revenue for my company, and I maintain that once I get there I will leave off marketing, prospecting, and client solicitation and reallocate that minor portion of my attention to even more focus on my clients. As I reflect today, the main feeling is that things are good, and they are going to get better. 9/17/2015 brief explanation: correlationIn discussions of policy and process, there is a phrase that gets a lot of play: "Correlation does not imply causation". One interpretation of that expression is that just because two (or more) things appear to happen or appear together regularly doesn't mean there is an explicit and clear connection between them. In finance, correlation is about mathOne aspect of the scientific and philosophic approach to portfolio design is recognition that there may be some connections between discrete pieces of a portfolio, and it is important to seek those out and consider their impacts.  Keeping this simple: a correlation measure can range from -1 to +1 (Negative 1 to positive 1). A correlation of +1 means that two things move together in perfect lockstep; a negative one means a perfect inverse relationship. Zero, right in the middle, suggests there is no implied or explicit relationship between the two things. In the chart above, the price of Apple's stock appears to be positively correlated with the S&P 500 for much of the last three years. don't assume too muchIn my practice, I try to look at statistical data like this with some skepticism to see if I can understand the underlying connection. If someone finds strong correlation between the height of a population and their preference for lattes over cappuccinos, I may do a little more digging to data manipulation. In the case shown above, however, it makes some sense that Apple and the S&P 500 tend to move together sometimes. For one thing, Apple is a member of that index, so Apple's movement does, itself, contribute to the overall performance of the index. Second, Apple is a disproportionately large contributor to the index.  Lastly, Apple is a huge company with a large presence in the US financial markets, and large companies tend, in general, to move in sync with other large companies. zero correlation raises diversityIf the goals for a given portfolio include a need for diversity (and risk sensitive portfolios should), the designer should run some testing on correlations among constituents.

9/2/2015 turns losses into wins?

So the market has taken a bit of a downturn in recent weeks. Blame what you like: China, Greece, oil prices are all among the possible culprits, but the net effect is the same -- stocks are down. As of this writing, the S&P 500 is down 7% for 2015.

There is not much that investors can do to avoid the bumps and bounces in the market -- the reality is that if you want the full potential upside of stocks, you must also accept the potential downsides. But, that is not to say that there aren't ways to make the most of the volatility and turn some negatives into positives. Here are a few actions that may make sense in your case:

tax loss harvesting

This option is only available in taxable accounts (not IRAs, 401ks, etc). The value proposition here is that realizing a capital loss on an investment may serve to lower your tax liability in the current tax year or some future tax year.

In very general terms, an individual may be able to claim up to $3000 per year in capital losses against their taxable income; for example, a person paying taxes at a 25% marginal rate could effectively lower their tax liability for the year by $750 ($3000 x 0.25). So in a period where stock and mutual fund prices may have dropped below the initial purchase price, it may in some circumstances make sense to sell, lock in the loss, and reinvest the proceeds in another investment that aligns with your goals and risk tolerance. Be careful and cognizant of "wash sale" rules.

rebalance

For rebalancing to be relevant, there is an assumption that you followed an asset allocation plan in the first place. In simple terms, asset allocation models suggest what percentage of an overall portfolio or goal should be invested in stocks, bonds, real estate, cash, or any number of possible categories. Over time, these percentages drift from the initial targets as the market bounces and does its thing. So rebalancing can bring the percentages back in line with the plan, or can be an opportunity to implement a new plan. In either case, big dips (or rises!) in the market will typically present an opportunity to rebalance...this may look like selling some things that are up and buying more of things that are down.

add cash

Often when a person opens an account or initially funds a goal they put in as much cash as they can at the time while maintaining an appropriate reserve or emergency fund. But over time, cash may build up in a checking or savings account in excess of what may be most appropriate for a given household's needs. While many people in the market may panic in a sell off, investors with excess cash may be in a position to make a strategic new or additional entry to the market. A price that is lower than it was before is not necessarily a good price, but in some cases a broad market sell off will create valuable opportunities.

In every case, seek qualified and professional advice before taking actions with tax, legal, and financial consequences.

|

AuthorDavid R Wattenbarger, president of DRW Financial Archives

June 2022

Categories |

RSS Feed

RSS Feed