|

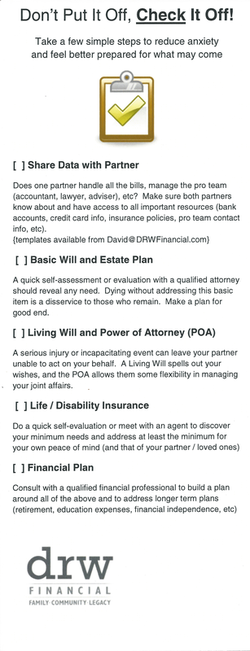

6/28/2013 Check it Off event was a success!Last night at Dish T'Pass in downtown Chattanooga we enjoyed great food, drink, and community. 15 or so new friends sampled a variety of hors d'oeuvres and chatted about the evening's topic: Checking Off a short list of basic "pre-planning" tasks.  It is just reality that people generally prefer to put off talking about things like death, illness, and disability - the idea of this event is to encourage folks to take a minute and just check these items off and move on to happier topics!

For the event last night, we had an attorney on hand to answer basic questions around estates and wills, an insurance agent to offer guidance on minimum coverage, and David from DRW Financial to chat about core planning concepts. Good food, nice conversation, and a little bit of valuable information - the ingredients for a successful event! Stay tuned for invitations to the next event in the "Social (study) Hour" series (tentatively scheduled for late July). 6/25/2013 The Market's Mood, in Pictures The chart above is a Year to Date look at what some call the "fear" metric, more formally known as the CBOE Volatility Index (VIX for short). The VIX is one way to measure current expectations of market volatility. The last few days have seemed pretty volatile, with the S&P dropping ~ 2.6% since June 19, with a few decent bumps up and down along the way. And here we have the same metric charted over a longer period of time, going back 10 years to see the trend coming into and exiting the crisis of '08. In both charts it is apparent that volatility (technically it is expected volatility) has spiked a bit lately. Will we see the spike continue up to levels last seen during those humps in 2010-2011? Or will we see the VIX settle back down in the low teens? And what does volatility imply for potential returns in the stock market? This final chart overlays the 10 year Volatility Index with the S&P 500 stock index. There is definitely some correlation between volatility and return, but not in a simplistic one to one kind of relationship. It would seem a reasonable guess that if uncertainty pushes volatility higher in the near future, that stock prices would fall a bit. Our perspective at DRW Financial is that the proper approach to potential volatility is to stay focused on each client's core concerns around investment objectives and risk tolerances, with a particular emphasis on liquidity concerns (volatility really informs liquidity risks).

6/20/2013 Yikes! What to do in a "down" market? The Dow is off more than 1% today, continuing a slide that began on the 18th. This is the kind of move that gets people's attention, and the financial media will all start squawking about whether this is the beginning of a major "correction", panic, sell-off, or similarly dramatic scenario.

So what should one do when faced with a day like today? What do prudent and sophisticated investors do here? Well, the one constant truth about the market is that it is made up of many different players with many different opinions and views, and so there are many diverse approaches for a day like today. It is even possible that there is more than one "right" answer. What DRW Financial does on a day like today is revisit our watch list for potential buying opportunities. Every week, whether the market is up, down, or sideways we refresh a screen of the whole equity market and pare down the 1000s of stocks out there to a few dozen that meet some very simple criteria. This smaller list features stocks from many different industries, a few different countries, and a small variety of economic profiles. If there are any on the list that meet all of our subjective conditions for "value", we buy them right away. Most, however, are 8/10 or 9/10 matches, with the current market price being the main obstacle. In those cases we set an alert at a target price to let us know when to refresh our analysis. Today is the kind of day that demands attention to the triggered alerts and a decision on whether to set new alerts at even lower prices or to turn a "watch list" stock into a "buy today!" stock. This style of evaluation applies mostly to our philosophy around individual equities (stocks) and less so to the more passive (or indexed) portions of client portfolios with a long term desire for exposure to a broad stock index. So what to do on a day like today? Take a deep breath or two, realize that markets will be volatile, and check your watch lists again to see if there are any new opportunities for value. ***This blog post is not a recommendation or solicitation to buy or sell a security, and is not intended as advice. Please consult an investment professional prior to making investment decisions, and/or thoroughly consider your own risk tolerance and investment objectives before taking action.*** 6/18/2013 Planning for...the end? Quick post today - I wanted to share this Ted Talk video I saw discussing a different facet of planning than we normally talk about here. Really, in my experience people don't often talk about this part of life at all or with anyone, but it struck me as powerful and thought provoking. So while not explicitly financial in content, please check out the video below as I see it as in keeping with DRW Financial's concern with Family | Community | Legacy: 6/14/2013 Some basics of dividend investing Should a portfolio include dividend paying stocks? What role do dividends play in an overall portfolio strategy? How should an investor go about choosing dividend payers? Today's post will attempt to shed some light on this corner of the market - but first, a short survey for you to share your thoughts: "Dividends" - the word has trickled out of the investment arena into our general language and shows up when people talk about any kind of choice that "paid off": the NFL draft pick that now "pays dividends", the college degree now "producing real dividends"...the general idea is that dividends are the result of a smart investment.

6/6/2013 Are bond yields about to flip out? It has become something of a truism in the financial press to point out that bond yields "can only rise" from here; this kind of statement is generally paired with an explanation that when bond yields rise, bond prices fall and will therefore hurt a portfolio holding bonds. The purpose of this post is not to suggest that bond yields won't rise in the near or distant future, or to make counter claims about rising yields and accounts holding bonds...what I seek to do here is offer some context and perspective. The last 6 months have shown a good bit of volatility, and end to end over that time the yield on the 10 year treasury has risen about 30% from ~ 1.6% up to 2.09%. No doubt that is a material move - in very general math that rise in yield would make the price of the 10 year bond fall by about 4.4%. Similarly, when the rate fell in the middle of the above chart, from just over 2% down to around 1.65%, bond prices would have risen significantly. What does it look like if you take a big step back? In this 5 year view, the recent pop-up in rates still looks big, but relative to some of the other bounces up and down it is relatively benign. That precipitous drop and subsequent spike in late '08 and early '09 represents a massive swing in value, on the order of ~ 15 - 17% of the value of the bond.

The main takeaway here is that interest rates are volatile, and that volatility impacts the value of portfolios holding bonds. What it doesn't mean is that bonds are necessarily too risky or a bad investment for certain clients; again, every investment option should be evaluated based on expected risks and returns within the investor's specific goals and time horizons. A couple of additional considerations, based solely on math:

And one consideration based on the nature of the markets:

6/4/2013 Cognitive BiasOur minds are wonderful things, and by and large they serve us pretty well to get us through life. Through a combination of "common sense" and basic learning, we are able to negotiate most of life's decisions, both small and large.

But there are some areas where our minds may let us down by jumping to the wrong conclusions too quickly...the term "cognitive bias" describes a tendency in our thinking that may lead us away from a rational or well reasoned conclusion. While cognitive biases exist outside of the realm of financial management, they definitely do show up consistently in the way people approach their money matters. I have saved a link on my browser to this collection of types of cognitive bias and I make a point of reviewing them on a regular basis to remind myself of the dangers in easy thinking. The list is not exhaustive, and there are other labels given to some of these concepts in other places, but image serves as a handy reference. One particular bias not named on that picture but that comes up often in finance is "confirmation bias". This bias shows up when a person has an idea or hypothesis, but only see supporting or confirming data while systematically overlooking or discounting contrary data. Basically, we like to be right, so the evidence that supports our thoughts is more attractive and tends to weigh more heavily in our own estimation than evidence that we may not be right. This bias can affect decisions to buy a specific investment or follow a particular strategy...for example an investor may see an ad for Coca-Cola while researching stocks and think "hey, maybe I should buy some Coke stock". While doing research on the company, they may then see an article mentioning that Warren Buffet likes Coca-Cola stock for his portfolio and - bam! - the investor may now feel that their thought is confirmed by Warren Buffet's opinion. The danger here is that each investor has a highly individual situation that ought to influence their view on risk, holding periods, diversification, etc. Coke stock may be a good fit for them or not, but the decision should flow from an understanding of their situation and that of the company, not whether a third party likes the stock for their portfolio. I should point out that cognitive bias does not necessarily lead to wrong conclusions, but may simply result in decisions that have not been fairly or thoroughly considered due to some shortcuts that our minds make (whether we are aware of those shortcuts or not!) |

AuthorDavid R Wattenbarger, president of DRW Financial Archives

June 2022

Categories |

RSS Feed

RSS Feed