|

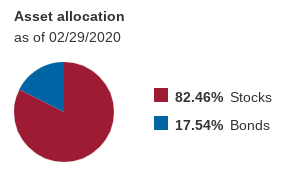

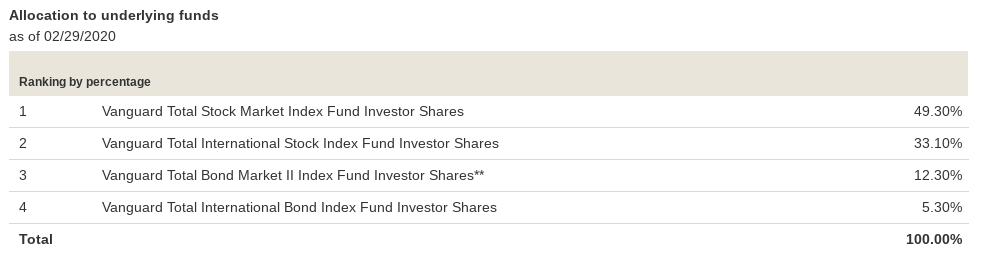

This post focused on target date funds, but could similarly apply to a "passive" portfolio of index funds that includes an allocation to bonds. Target retirement date mutual funds have become a mainstay of employer sponsored retirement plans (401k plans, for example), and many retail investors are choosing these options as well for their simplicity. The general idea of a target date fund (TDF) is that the fund holds a mix of assets - -mostly stocks and bonds -- in proportions that shift over time to lower the portfolio's expected volatility into the retirement date. In overly simplistic terms, this means that a far off target date fund will hold mostly stocks, and a very close target date fund will hold a relatively high proportion of bonds. For one example, consider the Vanguard Target Retirement 2040 fund, symbol VFORX:  This fund is meant for investors who believe that the year 2040 is likely when they will begin taking retirement distributions from their savings, or at least represent the amount of risk they want to take with those savings in the present. The Vanguard page for this fund also shows the underlying funds that make up the TDF:  For this blog post, I want to focus on the bond allocations within this fund. We can get more information on each, as they trade independently of the TDF under the symbols VTBIX and VTIBX. For further simplicity here, I will focus solely on the domestic fund, VTBIX. The rationale for holding bonds in a "diversified" portfolio along with stocks is that they historically represent different types of risk, and they typically respond differently to major shifts in the market's perception of risk. Often, in times of distress for the stock market, some investors will shift some of their money from stocks to bonds in pursuit of more stability or predictability, and this shift may raise the prices of bonds temporarily. And this general dynamic played out in the recent stock market correction related to the COVID 19 virus -- stocks fell, and at first bonds of almost every type rose. A subsequent wave of market reactions pushed US Treasury bonds higher still, but bonds of almost every other type (corporate bonds, municipal bonds, mortgage backed bonds, etc) fell a considerable amount as the market adjusted to consider the risk of those bond issuers "defaulting" on their obligations. For example, investors were forced to consider if bonds backed by a particular retailer or airline or car company would pay as expected if those companies were forced to close or go into bankruptcy. The chart below is clipped from CNBC, and shows the "year to date" price of the bond fund. That peak in early March, the sell off over the next two weeks, and the rebound up to today all match the general pattern of bonds in the market (except for US Treasuries which saw a much more muted sell off in mid-March)  This all leads to the inspiration for today's post: what does it mean to continue to hold bonds in the current market? Will bonds continue to provide the volatility dampening effect as per historical precedent? Pulling together fact sheets, prospectuses, and other resources on this particular Vanguard fund suggests that the current composition of underlying bonds is roughly 44% US Treasuries, with another 22% in mortgage backed bonds from "government sponsored entities" like Fannie Mae and Freddie Mac. In the current environment, the Federal Reserve is actively buying up those two categories of bonds to provide support and liquidity to the market -- this means, that all else held equal, the prices of those categories of bonds are being pushed higher and their yields pushed lower. For the VTBIX fund, the SEC Yield is currently just under 2%, and the distribution yield just over 2.5% -- but the underlying "yield to maturity" of the bonds held by the fund is ~ 1.70%, an average duration of more than 6 years, and an average maturity of more than 8 years. Taken all together, an investor holding this fund (or one very similar) may want to consider the possible paths for forward for economic gain in the fund, or the ways this holding may contribute to the overall performance of their portfolio. The "total return" of a bond or bond fund is made up of cash flows and price movement. As in the chart shown above, an investor buying the VTBIX fund on March 17 or so would have experienced a rise in price in addition to whatever dividends and interest the fund paid out during the holding period. And an investor holding that fund from March 7 to March 20 would have seen a meaningful shift to a lower price. A question I am asking myself and on behalf of my clients in this market is what may I rationally expect for bond and bond fund prices looking forward? The author holds no positions in the referenced funds, and is not soliciting a buy or sell of any security.

We ARE reviewing client investments in the current context of compressed interest rates and prospective returns on bonds and fixed income allocations. Comments are closed.

|

AuthorDavid R Wattenbarger, president of DRW Financial Archives

June 2022

Categories |

RSS Feed

RSS Feed